Perennial Real Estate Holdings (SGX: 40S) becomes the next target for privatization. However, not all the acquisition news is good for retail investors. In this article, Dr Tee will share the considerations by Big Boys or major shareholders to acquire or privatize a stock with Perennial as an example, with sharing of Reverse Takeover (RTO) stocks. You will learn the 47 undervalue Singapore property stocks which are profitable with over 50% price discount in asset value.

Interestingly, Perennial started its property business in year 2014 through Reverse Takeover (RTO) of St. James Holdings (entertainment business) which IPO in 2008. RTO is a quick way of “IPO” by acquiring an existing company which could be different business nature. A more famous example would be RTO of Berkshire Hathaway (NYSE: BRK) by Warren Buffett in year 1965, transforming an original textile manufacturing company into an insurance company.

There are quite a few property related stocks also get listed indirectly through RTO, eg. Hatten (SGX: PH0) and Centurion (SGX: OU8) / (HKEx: 6090). Therefore, a stock investor has to be careful in analysis of stock prices and business fundamental, viewing the RTO company as new IPO company, especially if the business is totally different with new management. So, the past performance (share prices and businesses) would not be meaningful references after RTO.

Perennial original IPO (under St. James) price was $12.95/share which shareholder would “lose” 95% if compare with price of $0.69/share before the privatization offer of $0.95/share. However, Years 2008-2014 was reflection of St James share prices and businesses. Perennial actual stock record should be from Years 2014-2020, share prices vary from about $1 to about $0.30 during the recent Covid-19 crisis. Perennial is not a giant stock but it is also not a junk stock. The bearish stock prices over the past 6 years are aligned with other Singapore property stocks (quite many are corrected by over 50% in share prices).

However, Perennial is relatively weaker than other Singapore property stocks. Therefore, the recent offer $0.95/share (despite lower than RTO price when Perennial first started in 2014) is considered attractive to investors after RTO. It is getting harder to delist or privatize a company in Singapore, therefore the offer must be significantly higher (38% for this case) to extend the current 82% shareholding to over 90% for mandatory takeover.

Perennial major shareholders include Wilmar (SGX: F34), together with other “big boys”, although 38% premium in offer price seems attractive but this amount (about $277M) will be paid by the new investor, Hopu Fund of China. Perennial has many good quality properties in both Singapore and China, last 1 year has significant cash from investing (sales of property), currently having $120M cash in the company which will be unlocked after privatization. More importantly, the company is undervalue, Price-to-Book (PB) ratio is 0.44 with 56% discount. This implies that the offer to 18% minority shareholders is technically “free” to major shareholders as Net Asset Value (NAV) is $1.58/share. Assuming PB of only 0.75 (25% discount) as market price (if were to sell the properties today), then the value gained from privatization would be $390M, more than enough to cover $277M cash.

Nevertheless, it is unlikely for Perennial to sell properties cheaply after privatization. With both high-quality commercial buildings and promising healthcare services, there is always an option for the company to get listed again (could be in other stock exchange) in future with higher valuation after another IPO or even RTO.

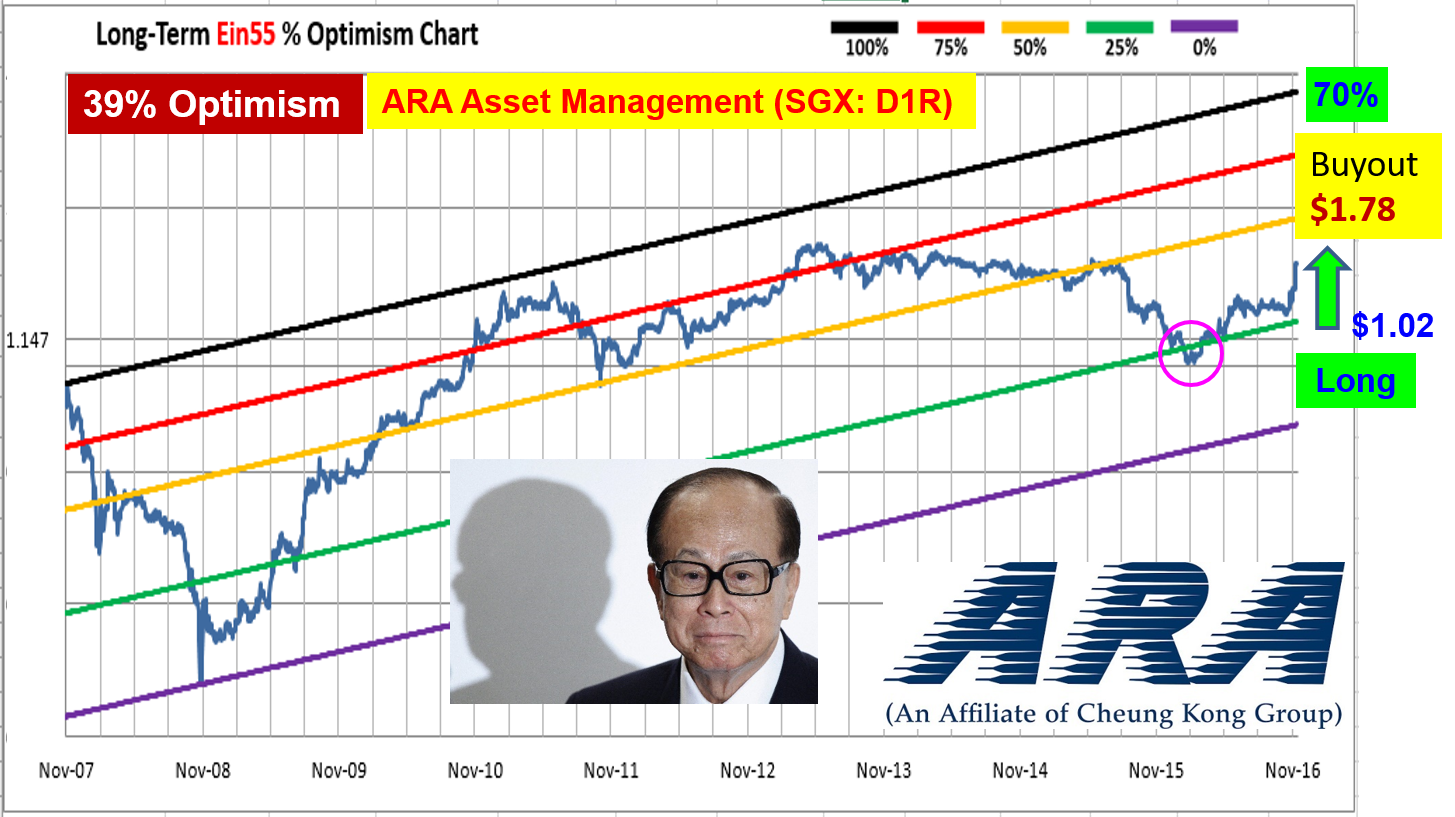

A few years ago, Wheelock Properties (SGX: M35) with over 50% discount in PB was acquired by parent company in Hong Kong, Wheelock Co (HKEx: 20), cash unlocked after acquisition was more than cash offered. Therefore, some cash rich companies have also tried to delist the company but not all the Big Boys are lucky. Previously, Challenger Technologies (SGX: 573) could not pass this barrier due to objection by minority shareholders as the company is fundamentally strong with cash rich. Breadtalk (SGX: CTN) acquisition offer was attractive partly due to severe stock crisis during Covid-10.

=====================================

There are 140 property & construction stocks in Singapore (REITs are excluded, see earlier articles by Dr Tee if interested: www.ein55.com/blog), many are undervalue but also losing money, “Buy Low” may simply get lower in share price.

3Cnergy (SGX: 502), A-Smart (SGX: BQC), AEI^ (SGX: AWG), AIMS Property (SGX: BVP), APAC Realty (SGX: CLN), Abterra (SGX: L5I), Acromec (SGX: 43F), Amara (SGX: A34), Amcorp Global (SGX: S9B), AnnAik (SGX: A52), Astaka (SGX: 42S), BBR (SGX: KJ5), BRC Asia (SGX: BEC), BlackGoldNatural (SGX: 41H), Boldtek (SGX: 5VI), Bonvests (SGX: B28), Boustead (SGX: F9D), Boustead Projects (SGX: AVM), Bukit Sembawang (SGX: B61), Bund Center (SGX: BTE), CSC (SGX: C06), CapitaLand (SGX: C31), Casa (SGX: C04), Chemical Industries (SGX: C05), China Great Land (SGX: D50), China International (SGX: BEH), China Real Estate (SGX: 5RA), China Yuanbang (SGX: BCD), Chip Eng Seng (SGX: C29), City Development (SGX: C09), DISA (SGX: 532), Debao Property (SGX: BTF), ETC Singapore (SGX: 1C0), Edition (SGX: 5HG), EnGro Corporation (SGX: S44), Fraser and Neave F&N (SGX: F99), Far East Orchard (SGX: O10), Figtree (SGX: 5F4), First Sponsor (SGX: ADN), Fragrance (SGX: F31), Frasers Property (SGX: TQ5), GYP Properties (SGX: AWS), Gallant Venture (SGX: 5IG), Golden Energy (SGX: AUE), Goodland (SGX: 5PC), GuocoLand (SGX: F17), HL Global Enterprises (SGX: AVX), Hatten Land (SGX: PH0), Heeton (SGX: 5DP), Hiap Hoe (SGX: 5JK), Hiap Seng (SGX: 510), Ho Bee Land (SGX: H13), Hock Lian Seng (SGX: J2T), Hong Fok (SGX: H30), Hong Lai Huat (SGX: CTO), Hong Leong Asia (SGX: H22), Hongkong Land USD (SGX: H78), Hor Kew (SGX: BBP), Huationg Global (SGX: 41B), Hwa Hong (SGX: H19), IPC Corp (SGX: AZA), ISOTeam (SGX: 5WF), Imperium Crown (SGX: 5HT), Jasper Investments (SGX: FQ7), KOP (SGX: 5I1), KSH (SGX: ER0), Keong Hong (SGX: 5TT), Keppel Corp (SGX: BN4), Keppel Reit (SGX: K71U), King Wan (SGX: 554), Koh Brothers (SGX: K75), Koon (SGX: 5DL), Kori (SGX: 5VC), LHN (SGX: 41O), Ley Choon (SGX: Q0X), Lian Beng (SGX: L03), Low Keng Huat (SGX: F1E), Lum Chang (SGX: L19), MMP Resources (SGX: F3V), MYP (SGX: F86), Metro (SGX: M01), OIO (SGX: KUX), OKH Global (SGX: S3N), OKP (SGX: 5CF), OneApex (SGX: 5SY), Oxley (SGX: 5UX), PSL (SGX: BLL), Pacific Century (SGX: P15), Pacific Star Development (SGX: 1C5), Pan Hong (SGX: P36), Pavillon (SGX: 596), Perennial Holdings (SGX: 40S), Pollux Properties (SGX: 5AE), PropNex (SGX: OYY), Raffles Infrastructure (SGX: LUY), Regal International (SGX: UV1), Renaissance United (SGX: I11), Rich Capital (SGX: 5G4), Roxy-Pacific (SGX: E8Z), Ryobi Kiso (SGX: BDN), SHS (SGX: 566), SLB Development (SGX: 1J0), SP Corporation (SGX: AWE), Sasseur Reit (SGX: CRPU), Second Chance (SGX: 528), Sin Heng Mach (SGX: BKA), Sinarmas Land (SGX: A26), SingHaiyi (SGX: 5H0), SingHoldings (SGX: 5IC), Singapore-eDev (SGX: 40V), Sinjia Land (SGX: 5HH), Soilbuild Construction Group (SGX: S7P), Starland (SGX: 5UA), Straits Trading (SGX: S20), Swee Hong (SGX: QF6), Sysma (SGX: 5UO), TA (SGX: PA3), TTJ (SGX: K1Q), Tai Sin Electric (SGX: 500), Thakral (SGX: AWI), Thomson Medical Group (SGX: A50), Tiong Seng (SGX: BFI), Top Global (SGX: BHO), Tosei (SGX: S2D), Transcorp (SGX: T19), Tritech (SGX: 5G9), UIC (SGX: U06), UOA (SGX: EH5), UOL (SGX: U14), USP Group (SGX: BRS), Vibrant Group (SGX: BIP), Wee Hur (SGX: E3B), Wing Tai (SGX: W05), Yanlord Land (SGX: Z25), Yeo Hiap Seng (SGX: Y03), Ying Li International (SGX: 5DM), Yoma Strategic (SGX: Z59), Yongmao (SGX: BKX), Yongnam (SGX: AXB), Yorkshine (SGX: MR8).

There are only 47 undervalue (PB < 0.5) Singapore property stocks are profitable in the last 1 year, including Perennial.

From table below, we could see property stocks with PB = $/NAV from 0.13 to 0.5. Despite over 50% discount in share prices over NAV with profitable business, majority of stocks are not giant stocks. An undervalue stock may remain undervalue for a long term, sometimes may be even acquired by Big Boys at low optimism price in a bearish stock market (弱肉强食).

| No | Name | Ticker | PB = Price/NAV | ROE (%) |

| 1 | Huationg Global | 41B | 0.13 | 5.3 |

| 2 | Hor Kew | BBP | 0.16 | 1.0 |

| 3 | Top Global | BHO | 0.18 | 0.2 |

| 4 | Casa | C04 | 0.18 | 4.5 |

| 5 | ETC Singapore | 1C0 | 0.22 | 5.8 |

| 6 | Hong Lai Huat | CTO | 0.23 | 1.4 |

| 7 | Hong Fok | H30 | 0.24 | 5.6 |

| 8 | Koh Bros | K75 | 0.24 | 1.9 |

| 9 | SP Corp | AWE | 0.24 | 4.5 |

| 10 | Pavillon | 596 | 0.24 | 1.1 |

| 11 | HongkongLand | H78 | 0.25 | 0.5 |

| 12 | Heeton | 5DP | 0.25 | 3.0 |

| 13 | HL Global Ent | AVX | 0.27 | 1.1 |

| 14 | Tiong Seng | BFI | 0.28 | 4.0 |

| 15 | Lian Beng | L03 | 0.28 | 4.7 |

| 16 | China Intl | BEH | 0.30 | 5.6 |

| 17 | Sinarmas Land | A26 | 0.30 | 15.1 |

| 18 | AnnAik | A52 | 0.31 | 3.3 |

| 19 | TTJ | K1Q | 0.34 | 2.3 |

| 20 | Vibrant Group | BIP | 0.34 | 3.8 |

| 21 | Keong Hong | 5TT | 0.36 | 7.3 |

| 22 | Far East Orchard | O10 | 0.37 | 2.1 |

| 23 | Chemical Ind | C05 | 0.38 | 8.8 |

| 24 | Pan Hong | P36 | 0.38 | 15.4 |

| 25 | Ho Bee Land | H13 | 0.39 | 9.4 |

| 26 | Hiap Hoe | 5JK | 0.39 | 2.9 |

| 27 | King Wan | 554 | 0.40 | 1.6 |

| 28 | LHN | 41O | 0.40 | 8.3 |

| 29 | Thakral | AWI | 0.41 | 6.7 |

| 30 | Metro | M01 | 0.41 | 5.6 |

| 31 | Yanlord Land | Z25 | 0.41 | 11.9 |

| 32 | Wing Tai | W05 | 0.42 | 1.3 |

| 33 | EnGro | S44 | 0.42 | 4.7 |

| 34 | Bonvests | B28 | 0.43 | 0.4 |

| 35 | Kori | 5VC | 0.43 | 0.2 |

| 36 | GuocoLand | F17 | 0.43 | 6.1 |

| 37 | Perennial Hldgs | 40S | 0.44 | 0.1 |

| 38 | Low Keng Huat | F1E | 0.44 | 1.9 |

| 39 | Straits Trading | S20 | 0.44 | 5.6 |

| 40 | UIC | U06 | 0.44 | 8.3 |

| 41 | Pollux Prop | 5AE | 0.44 | 2.5 |

| 42 | SingHaiyi | 5H0 | 0.44 | 0.1 |

| 43 | Wee Hur | E3B | 0.44 | 8.8 |

| 44 | SingHoldings | 5IC | 0.45 | 15.4 |

| 45 | Lum Chang | L19 | 0.45 | 9.1 |

| 46 | Chip Eng Seng | C29 | 0.48 | 3.6 |

| 47 | Hong Leong Asia | H22 | 0.50 | 4.5 |

Based on Dr Tee criteria, from the 47 shortlisted Singapore property stocks above, only 8 are giant stocks. A few undervalue property giant stocks were mentioned in earlier articles (see https://www.ein55.com/tag/property-stocks/), eg. GuocoLand (SGX: F17) and Hongkong Land (SGX: H78). However, not all major shareholders are interested of delisting the undervalue property stocks because some are family owned for decades, value of shares may recover to NAV only when they are ready to sell one day. It may be hard for Big Boys or external funds to acquire. For example, Li Ka-shing was hoping to acquire Hongkong Land in 1980s but was rejected with tighter control by parent stock from Jardine Group, Jardine Matheson Holdings JMH (SGX: J36) and Jardine Strategic Holdings JSH (SGX: J37).

Property stocks (both Singapore and regional stock markets in Malaysia and Hong Kong, etc) are cyclic in nature. Therefore, market cycle investing strategy is required with alignment to Optimism Strategies to Buy Low Sell High, as well as good understanding the local property market cycle. Property stocks is an integration of stock and property markets, knowledge in both markets are required to enhance the chances of success in investing.

Undervalue stocks are bonus for additional safety (huge discount in price below value with high quality asset of property), especially for property stocks but mainly suitable for patient long term investors. A smart investor may integrate undervalue stocks with dividend strategies. This is suitable for passive income investing, similar to property investment, an alternative to REITs but an investor of property stock (non-REIT) could also enjoy the capital gains (or suffer the losses) of property valuations, not just the rental income. For example, many property stocks (including Hongkong Land) are lower in valuation (affecting earnings) in Hong Kong but cash flow is not much affected.

So, reading between the lines for 3 financial reports (Income Statement, Balance Sheet, Cash Flow statement) are important to fully understand the property stocks, especially property development company has different project cycles which may last a few years, resulting in cyclic property business results and stock prices. So, Level Analysis of Level 1 (individual stock), Level 2 (Property Sector), Level 3 (local country) and Level 4 (world economy and global stock market) are required.

There are hundreds of global property giant stocks (may not need to be undervalue), an investor just needs to select 1 of Top 10 property stocks, adding to a dream team stock portfolio of 10-20 giant stocks (eg. best stock in each sector, min 3 sectors: REIT, Healthcare, F&B, Oil & Gas, Bank, Commodity, Insurance, etc). Value investors may own these 10-20 companies at undervalue price to work for us through shareholding, generating incomes (capital gains of higher share prices and dividend payment) over a lifetime (even beyond own retirement) with yearly review of giant stock status to continue the holding. So, every stock crisis is an opportunity to Buy Low with condition that it must be a giant stock.

There are 30 STI index component stocks including property stocks: CapitaLand, Hongkong Land, City Development and UOL (investor has to focus only on giant stocks for investing):

DBS Bank (SGX: D05), Singtel (SGX: Z74), OCBC Bank (SGX: O39), UOB Bank (SGX: U11), Wilmar International (SGX: F34), Jardine Matheson Holdings JMH (SGX: J36), Jardine Strategic Holdings JSH (SGX: J37), Thai Beverage (SGX: Y92), CapitaLand (SGX: C31), Ascendas Reit (SGX: A17U), Singapore Airlines (SGX: C6L), ST Engineering (SGX: S63), Keppel Corp (SGX: BN4), Singapore Exchange (SGX: S68), Hongkong Land (SGX: H78), Genting Singapore (SGX: G13), Mapletree Logistics Trust (SGX: M44U), Jardine Cycle & Carriage (SGX: C07), Mapletree Industrial Trust (SGX: ME8U), City Development (SGX: C09), CapitaLand Mall Trust (SGX: C38U), CapitaLand Commercial Trust (SGX: C61U), Mapletree Commercial Trust (SGX: N2IU), Dairy Farm International (SGX: D01), UOL (SGX: U14), Venture Corporation (SGX: V03), YZJ Shipbldg SGD (SGX: BS6), Sembcorp Industries (SGX: U96), SATS (SGX: S58), ComfortDelGro (SGX: C52).

=====================================

Drop by Dr Tee free 4hr investment course to learn how to position in global giant stocks with 10 unique stock investing strategies, knowing What to Buy, When to Buy/Sell.

Learn further from Dr Tee valuable 7hr Online Course, both English (How to Discover Giant Stocks) and Chinese (价值投资法: 探测强巨股) options, specially for learners who prefer to master stock investment strategies of over 100 global giant stocks at the comfort of home.

You are invited to join Dr Tee private investment forum (educational platform, no commercial is allowed) to learn more investment knowledge, interacting with over 9000 members.