Information Technology (IT) is everywhere in modern world, a stock with strong IT related business would have bright future for investment. Therefore, an investor may consider 28 IT stocks in Singapore, especially those defensive growth stocks.

In this article, you will learn from Dr Tee on 4 Singapore IT Giant Stocks which are efficient in making money with economic moat but having mixed impacts during COVID-19 stock crisis. Bonus for readers who could read every words of the entire article: 7 global IT giant stocks.

1) IT Retail Giant Stock

– Challenger Technologies (SGX: 573)

2) Software Giant Stock

– Silverlake Axis (SGX: 5CP)

3) Data Center Giant REITs

– Keppel DC Reit (SGX: AJBU)

– Mapletree Industrial Trust (SGX: ME8U)

Nearly everyone of us needs certain IT services in our daily lives, eg. when reading Dr Tee article here with common online platforms which are also global giant stocks: Google (NASDAQ: NYSE), Facebook (NASDAQ: FB), etc. Most global IT giant stocks are from US but there are still some good local IT giant stocks in Singapore worth consideration for investment.

There are 28 IT Stocks in Singapore, making money with Information Technology (通风报讯):

Alpha Energy Holdings (SGX: 5TS), Alset International (SGX: 40V), Artivision Technologies (SGX: 5NK), Asiatravel.com Holdings (SGX: 5AM), A-Smart Holdings (SGX: BQC), Azeus Systems Holdings (SGX: BBW), Boustead Singapore Limited (SGX: F9D), Captii (SGX: AWV), Challenger Technologies (SGX: 573), CSE Global (SGX: 544), DISA (SGX: 532), International Press Softcom (SGX: 571), ISDN Holdings (SGX: I07), Keppel DC Reit (SGX: AJBU), Koyo International (SGX: 5OC), M Development (SGX: N14), Mapletree Industrial Trust (SGX: ME8U), New Silkroutes Group (SGX: BMT), New Wave Holdings (SGX: 5FX), PEC (SGX: IX2), Plato Capital (SGX: YYN), Procurri Corporation (SGX: BVQ), Rich Capital Holdings (SGX: 5G4), Silverlake Axis (SGX: 5CP), SinoCloud Group (SGX: 5EK), Stratech Group (SGX: BRR), Synagie Corp (SGX: V2Y), YuuZoo Networks Group Corp (SGX: AFC).

These 28 IT stocks are also related in businesses to 53 Electronics Technology Stocks in Singapore:

AEM Holdings (SGX: AWX), Accrelist Limited (SGX: QZG), Acma Limited (SGX: AYV), Adventus Holdings (SGX: 5EF), Allied Technologies Limited (SGX: A13), Amplefield Limited (SGX: AOF), Avi Tech Electronics (SGX: BKY), Ban Leong Technologies (SGX: B26), CDW Holding (SGX: BXE), CFM Holdings (SGX: 5EB), CPH Limited (SGX: 539), Chuan Hup Holdings (SGX: C33), Creative Technology (SGX: C76), Datapulse Technology (SGX: BKW), Dragon Group International (SGX: MT1), Dutech Holdings (SGX: CZ4), Ellipsiz Limited (SGX: BIX), Excelpoint Technology (SGX: BDF), Frencken Group (SGX: E28), Global Invacom Group (SGX: QS9), GP Industries (SGX: G20), Global Testing Corporation (SGX: AYN), Grand Venture Technology (SGX: JLB), HGH Holdings (SGX: 5GZ), Hu An Cable Holdings (SGX: KI3), JEP Holdings (SGX: 1J4), Jadason Enterprises (SGX: J03), Karin Technology Holdings (SGX: K29), Libra Group (SGX: 5TR), Manufacturing Integration Technology (SGX: M11), Maruwa Yen1k (SGX: M12), MeGroup Limited (SGX: SJY), Micro-Mechanics Holdings (SGX: 5DD), Plastoform Holdings (SGX: AYD), Polaris Limited (SGX: 5BI), Powermatic Data Systems (SGX: BCY), Renaissance United (SGX: I11), SEVAK Limited (SGX: BAI), SUTL Enterprise (SGX: BHU), Serial System (SGX: S69), Shinvest Holding (SGX: BJW), Sunright Limited (SGX: S71), Sunrise Shares Holdings (SGX: 581), TT International (SGX: T09), Thakral Corporation (SGX: AWI), The Place Holdings (SGX: E27), Trek 2000 International (SGX: 5AB), Valuetronics Holdings (SGX: BN2), Venture Corporation (SGX: V03), Willas-Array Electronics Holdings (SGX: BDR), World Precision Machinery (SGX: B49).

From the table sorted below for 28 Singapore IT stocks, only half are profitable (17 / 28 stocks were making money in businesses last year). Therefore, careful choices of giant IT stocks are critical, some are at lower optimism share prices due to either stock market fear or actual business is affected during COVID-19 pandemic.

Most Singapore IT stocks don’t pay dividend (only 11 / 28 stocks pay dividend). Even if they do, for example, CSE Global (SGX: 544) and Boustead Singapore (SGX: F9D) with over 4% dividend yield, are not good dividend stocks due to weaker business fundamental.

Only 1/3 of IT stocks (9 / 28) have Price-to-Book ratio ($ / NAV = PB) < 1 with discount over asset but majority do not have high quality asset related to cash or properties.

For most local and global IT stocks, main strategy would be growth investing or momentum trading, therefore business growth is much more important than undervalue price or dividend payment.

| No | Name | Code | ROE (%) | Dividend Yield (%) | PB = Price /NAV |

| 1 | Alpha Energy Holdings | 5TS | – | – | 3.64 |

| 2 | Alset International | 40V | – | – | 3.78 |

| 3 | Artivision Technologies | 5NK | 7.0 | – | -0.77 |

| 4 | Asiatravel.com Holdings | 5AM | 0.4 | – | 2.62 |

| 5 | A-Smart Holdings | BQC | – | – | 3.97 |

| 6 | Azeus Systems Holdings | BBW | – | 2.7 | 2.30 |

| 7 | Boustead Singapore Limited | F9D | 5.1 | 4.3 | 0.99 |

| 8 | Captii | AWV | 26.8 | 3.7 | 0.27 |

| 9 | Challenger Technologies | 573 | – | 3.3 | 1.41 |

| 10 | CSE Global | 544 | 0.7 | 5.7 | 1.30 |

| 11 | DISA | 532 | 12.4 | – | 1.11 |

| 12 | International Press Softcom | 571 | – | – | 0.69 |

| 13 | ISDN Holdings | I07 | – | 1.0 | 1.04 |

| 14 | Keppel DC Reit | AJBU | 12.6 | 2.5 | 2.55 |

| 15 | Koyo International | 5OC | 5.2 | 1.3 | 0.77 |

| 16 | M Development | N14 | – | – | 0.87 |

| 17 | Mapletree Industrial Trust | ME8U | 10.3 | 3.5 | 1.94 |

| 18 | New Silkroutes Group | BMT | 3.2 | – | 0.61 |

| 19 | New Wave Holdings | 5FX | 13.6 | – | 0.90 |

| 20 | PEC | IX2 | 18.5 | 1.2 | 0.58 |

| 21 | Plato Capital | YYN | 17.0 | – | 0.18 |

| 22 | Procurri Corporation | BVQ | – | – | 1.82 |

| 23 | Rich Capital Holdings | 5G4 | – | – | 1.36 |

| 24 | Silverlake Axis | 5CP | 22.8 | 2.1 | 3.18 |

| 25 | SinoCloud Group | 5EK | 27.1 | – | 1.00 |

| 26 | Stratech Group | BRR | – | – | -0.49 |

| 27 | Synagie Corp | V2Y | 2.2 | – | 7.24 |

| 28 | YuuZoo Networks Group Corp | AFC | 15.2 | – | -3.49 |

There are only 2 IT related stocks (Mapletree Industrial Trust, following by Keppel DC Reit would be included soon by end of 2020) which are also listed in 30 STI component stocks:

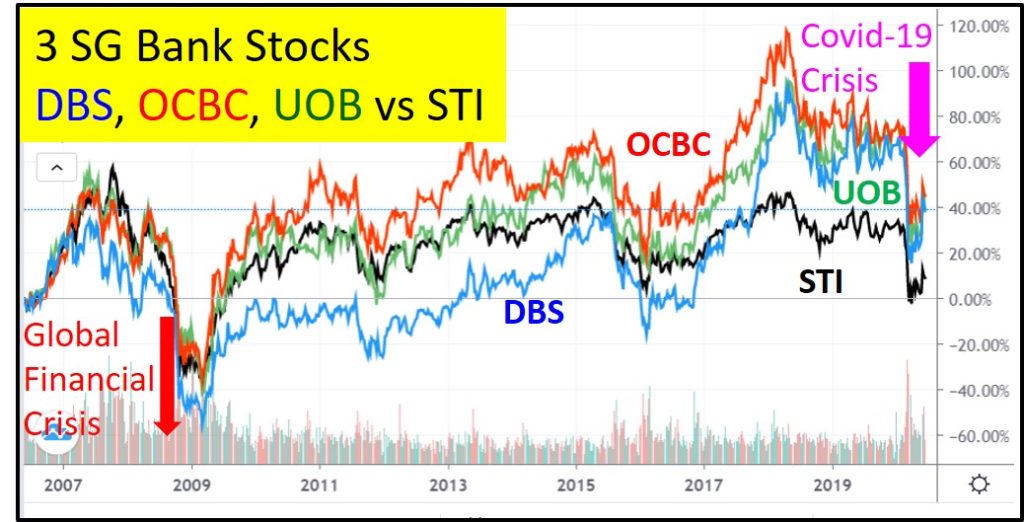

DBS Bank (SGX: D05), Singtel (SGX: Z74), OCBC Bank (SGX: O39), UOB Bank (SGX: U11), Wilmar International (SGX: F34), Jardine Matheson Holdings JMH (SGX: J36), Jardine Strategic Holdings JSH (SGX: J37), Thai Beverage (SGX: Y92), CapitaLand (SGX: C31), Ascendas Reit (SGX: A17U), Singapore Airlines (SGX: C6L), ST Engineering (SGX: S63), Keppel Corp (SGX: BN4), Singapore Exchange (SGX: S68), HongkongLand (SGX: H78), Genting Singapore (SGX: G13), Mapletree Logistics Trust (SGX: M44U), Jardine Cycle & Carriage (SGX: C07), Mapletree Industrial Trust (SGX: ME8U), City Development (SGX: C09) , CapitaLand Mall Trust (SGX: C38U), CapitaLand Commercial Trust (SGX: C61U), Mapletree Commercial Trust (SGX: N2IU), Dairy Farm International (SGX: D01), UOL (SGX: U14), Venture Corporation (SGX: V03), YZJ Shipbldg SGD (SGX: BS6), Sembcorp Industries (SGX: U96), SATS (SGX: S58), ComfortDelGro (SGX: C52).

An investor has to be selective in investing as many IT stocks in Singapore are weak (buy low may get lower in share price due to weak business, especially in a bearish stock market), despite they belong to a promising IT industry but the competition is too intense, only some IT stocks could be profitable in longer term.

Here, let’s focus on 4 Singapore IT giant stocks over 3 main categories:

1) IT Retail Giant Stock

– Challenger Technologies (SGX: 573)

Challenger Technologies has many IT retail stores in Singapore, business has been growing. In Year 2019, the acquisition offer by major shareholders was not successful due to joint effort of smart minority shareholders with over 10% objection votes. As a result, Singapore can still keep this giant stock, especially the company has strong cash flow, able to pay consistent dividend in the past, suitable for longer term investing.

However, over the past 2 years, Challengers Technologies has reduced on the dividend payment (unsure if this may be a move to discourage longer term investing, especially after the acquisition was not successful). In fact, the company is defensive in both share prices and business, not affect affected during COVID-19 compared with peers.

So, Challenger Technologies is transformed from a dividend stock (defender) in the past to a growth stock (midfielder with moderate dividend and capital gains). Current share price is at lower optimism level but it may not be suitable for traders due to sideways prices (which is better than most bearish Singapore stocks). Since this is not a REIT, major shareholders have the power to change the dividend payout policy each year, making it less attractive to longer term investors for holding, perhaps a higher chance for acquisition again in future if both the capital gains and dividends are limited in medium term.

In Singapore, besides Challenger Technologies, consumers may also go to Harvey Norman IT stores which is listed in Australia stock market (ASX: HVN). Harvey Norman is as strong as Challenger Technologies, another option for global IT giant stock investing. Even during crisis such as COVID-19, their businesses are doing better as there are online sales channel, demand is supported by more IT users.

2) Software Giant Stock

– Silverlake Axis (SGX: 5CP)

Silverlake Axis provides software solutions and services to the banking, insurance, payment, retail and logistics industries. It is a leader for backend software to many banks in Southeast Asia (Malaysia, Singapore, Indonesia, etc). Banks usually don’t easily change the supplier of financial software for safety and stability, therefore Silverlake Axis has economic moat in high switching cost.

In Year 2015, there was allegation reported on questionable high profitability of company, even if there is no confirmation, resulting in significant correction of share price from peak of over $1/share, bearish share prices continue in the past few years to about 20% of peak share price during COVID-19 stock crisis, currently at low optimism. Silverlake Axis business is affected during pandemic but this is reasonable compared with peers and clients (most banks have weaker businesses during COVID-19).

Financial reports are key consideration for investors, therefore any doubt (even not confirmed) could create unwanted market fear, resulting in falling of share prices. Another recent example is Best World International (SGX: CGN) which also reported very good financial results, attracting questions on reliability of business performance. Even during the stock suspension period, Best World continues to report expected good financial results.

So, for a giant stock, besides good business fundamental, it is important for management to pay more attention on public communication, be transparent in financial reports, especially on grey areas. Luckin Coffee (NASDAQ: LK, forced to be delisted) was a negative example that a “strong fundamental” company ends up in scandal of deceiving global investors (including GIC of Singapore) with manipulated financial reports. Integrity of management is key for a giant stock but it is very hard to measure as greed could drive a business to different direction. Sometimes under the pressure of investors expectation, some management of companies may choose shortcut to achieve early “success” with creative accounting. So, stock investors have to read between the lines for financial reports, reviewing each potential allegation or rumors if there is any.

Overall, assuming truthful financial reports over the past decade, Silverlake Axis is a reasonable strong fundamental stock at low optimism but it is very cyclical in nature, an investor needs to have holding power when buying at low optimism.

3) Data Center Giant REITs

– Keppel DC Reit (SGX: AJBU)

– Mapletree Industrial Trust (SGX: ME8U)

Both Keppel DC Reit and Mapletree Industrial Trust (MIT) are data center REITs, benefiting from increasing demand in internet era for data storage to keep critical and sensitive information for clients in different countries globally. Data center business has strong economic moat (high switching cost) and predictable in income generation, supported by clients who are financially strong with internet related businesses.

Keppel DC Reit is mainly on data center business, growth in business with strong cash, could double the dividend in about 4 years, much stronger than most dividend stocks and REITs which need 8-10 years to double the dividend payment. However, this strong growth has attracted competition globally, therefore the high growth rate in share prices and businesses would slow down in longer term. The share price was corrected by about 20% during COVID-19 stock crisis but quickly recover to new historical high prices, currently at high optimism. So, the stock is more suitable for momentum trading as the dividend yield is less than 3%, trend-following trading strategy may be applied. Keppel DC Reit would be the next in line for new 30 STI component stock, replacing the empty slot when CapitaLand Mall Trust (SGX: C38U) and CapitaLand Commercial Trust (SGX: C61U) are merged by end of 2020, with new opportunity for higher upside in share prices with more fund managers support.

Mapletree Industrial Trust has acquired 14 more data centers in US, overall business contribution with data center is about 40%, would help to accelerate the future growth of company. The company share price and business performance are similar to Keppel DC Reit, but it is more gradual in growth. After replacing Singapore Press Holding, SPH (SGX T39) as the latest 30 STI component stock in Year 2020, MIT share price is supported further (currently at high optimism) with more institutional investors. MIT may be considered as midfielder with capital gains and moderate 3.7% dividend yield, currently more suitable for trend-following trading or growth investing due to higher optimism prices.

Both Keppel DC Reit and MIT are stronger growth REITs compared with 52 Singapore REITs and Business Trusts which are mainly positioned for dividend investing (investor has to focus only on giant stocks for investing):

AIMS APAC Reit (SGX: O5RU), ARA Hospitality Trust USD (SGX: XZL), ARA LOGOS Logistics Trust (SGX: K2LU), Ascendas Reit (SGX: A17U), Ascendas India Trust (SGX: CY6U), Ascott Trust (SGX: HMN), Asian Pay Tv Trust (SGX: S7OU), BHG Retail Reit (SGX: BMGU), CapitaLand Commercial Trust (SGX: C61U), CapitaLand Mall Trust (SGX: C38U), CapitaLand Retail China Tr (SGX: AU8U), CDL Hospitality Trust (SGX: J85), Cromwell Reit EUR (SGX: CNNU), Cromwell Reit SGD (SGX: CSFU), Dasin Retail Trust (SGX: CEDU), Eagle Hospitality Trust USD (SGX: LIW), EC World Reit (SGX: BWCU), Elite Commercial Reit (SGX: MXNU), ESR-REIT (SGX: J91U), Far East Hospitality Trust (SGX: Q5T), First Reit (SGX: AW9U), Frasers Centrepoint Trust (SGX: J69U), Frasers Hospitality Trust (SGX: ACV), Frasers Logistics & Commercial Trust (SGX: BUOU), FSL Trust (SGX: D8DU), HPH Trust SGD (SGX: P7VU), HPH Trust USD (SGX: NS8U), IREIT Global (SGX: UD1U), Keppel Infrastructure Trust (SGX: A7RU), Keppel Pacific Oak US REIT (SGX: CMOU), Keppel DC Reit (SGX: AJBU), Keppel Reit (SGX: K71U), Lendlease Reit (SGX: JYEU), Lippo Malls Trust (SGX: D5IU), Manulife Reit (SGX: BTOU), Mapletree Commmercial Trust (SGX: N2IU), Mapletree Industrial Trust (SGX: ME8U), Mapletree Logistics Trust (SGX: M44U), Mapletree North Asia Commercial Trust (SGX: RW0U), NetLink NBN Trust (SGX: CJLU), OUE Commercial Reit (SGX: TS0U), ParkwayLife Reit (SGX: C2PU), Prime US Reit (SGX: OXMU), RHT HealthTrust (SGX: RF1U), Sabana Reit (SGX: M1GU), Sasseur Reit (SGX: CRPU), Soilbuild Business Space Reit (SGX: SV3U), SPH Reit (SGX: SK6U), Starhill Global Reit (SGX: P40U), Suntec Reit (SGX: T82U), United Hampshire US Reit (SGX: ODBU).

=======================================

In fact, a company does not need to pay dividend to be a giant stock. Warren Buffett Berkshire Hathaway (NYSE: BRK.A / BRK.B) did not pay dividend for the past decades, retained earnings are accumulated, making it the most expensive stock in the world. So, a company value can be evaluated from both past and future earnings and cash flow.

Nearly every company or investor needs IT except for Warren Buffett. Many years ago, Bill Gates (founder of Microsoft, NASDAQ: MSFT, also a global IT giant stock) was trying to persuade his good friend (who supports his charity fund), Warren Buffett, to accept application of computer, at least to manage his stock portfolio. Warren Buffett joked that he only has 1 stock (which is Berkshire Hathaway), therefore no need computer at all. In reality, main contributor of Berkshire revenue now is from world largest IT giant stock, Apple Inc (NASDAQ: AAPL). Warren Buffett regrets of not able to investing in Amazon.com (NASDAQ: AMZN), another US IT giant stock in earlier stage with lower prices. For growth investing, an investor may not need to buy low but need to invest more during stock crisis, leveraging on power of time to compound the share prices with condition the strong growth businesses are sustainable.

Although Warren Buffett is not IT savvy, he could read the financial reports of Apple, understanding his strong economic moat to continue to make money as a market leader, at least for the current decade. Indeed, IT is beneficial to businesses but an investor may not need to be high tech person to invest in high tech stocks. However, since technology sector is very dynamic, especially for information technology, new or disruptive technology could take the lead at the right time. For example, Zoom Video Communications (NASDAQ: ZM) is a promising young IT stock, by right needs another 5-10 more years to become a proven giant stock but the process is shortened to months with unexpected help of COVID-19 crisis with millions of new users including Dr Tee during pandemic.

===================================

There are over 1500 giant stocks in the world based on Dr Tee criteria, choice of 10 Dream Team giant stocks have to align with one’s unique personality, eg. for shorter term trading (eg. momentum or swing trading) or longer term investing (cyclic investing, undervalue investing or growth investing). Readers should not just “copy and paste” any stock (What to Buy, When to Buy/Sell) as successful action taking requires deeper consideration (LOFTP strategies – Level / Optimism / Fundamental / Technical / Personal Analysis) which you could learn further from Dr Tee Free 4-hr Webinar.

Drop by Dr Tee free 4hr webinar (learning at comfort of home with Zoom) to learn how to position in global giant stocks during COVID-19 stock crisis with 10 unique stock investing strategies, knowing What to Buy, When to Buy/Sell.

Zoom will be started 30 min before event, bonus talk (Q&A on any investment topics from readers) for early birds. There are many topics we will cover in this 4hr webinar, Dr Tee can have more time for Q&A if you could stay later after the webinar.

Dr Tee will cover over 20 case studies, Singapore giant stocks, eg. CapitaLand Mall Trust (SGX: C38U), Singapore Exchange (SGX: S68), Keppel Corp (SGX: BN4), Top Glove (SGX: BVA), Jardine Matheson Holdings JMH (SGX: J36), Vicom (SGX: WJP) and many others, Malaysia giant stocks, Hong Kong giant stocks and US giant stocks, both long term investing and short term trading.

There are limited tickets left for this 4hr free webinar, please ensure 100% you could join when register: www.ein55.com